Marshall McLuhan said the medium is the message. In search terms, Google has been both for the best part of two decades. The way people find things, the way businesses get found, the way the commercial web is structured — all of it built around one platform that held 90%+ of global search market share for nearly ten years without serious interruption.

Then AI arrived and the consensus was that Google was finished. ChatGPT would replace search. GEO was the new SEO. The ten blue links were dead. Every LinkedIn post had a hot take. Every conference had a panel. Every agency rebranded something.

The data tells a different story.

Five years of market share — what actually happened

Google's global search market share was remarkably stable from 2020 through 2023 — holding between 91% and 93% throughout. The peak was 92.9% in 2023. Then it started softening. By late 2024 it had dipped below 90% for the first time since 2015 — 89.34% in October, 89.99% in November, 89.73% in December.

Three months. Twelve months of headlines about Google's existential crisis produced three months of sub-90% market share — and then Google launched AI Mode in mid-2025 and the share stabilised back toward 90%. Revenue kept growing throughout. The market decided Google was not dying.

| Year | Google global share | Bing global share | Google ad revenue |

|---|---|---|---|

| 2020 | ~92% | ~2.5% | ~$104bn |

| 2021 | ~92% | ~3% | ~$149bn |

| 2022 | ~92% | ~3% | ~$163bn |

| 2023 | 92.9% (peak) | ~3% | ~$175bn |

| 2024 | ~89.5% (dipped below 90%) | ~4% | ~$198bn |

| 2025/26 | ~90% (stabilised) | ~4% | ~$252bn |

Bing grew from roughly 2.5% to 4% over the same period — real growth, largely driven by AI integration with Copilot, but nowhere near threatening Google's position. In the US it sits at around 8.5% — more significant, but still a distant second.

ChatGPT: the actual numbers

ChatGPT processes around 2.5 billion messages per day, of which approximately 887 million are search-equivalent queries. Google processes 16.4 billion searches per day. That is not a comparison that suggests displacement.

As a referral source, AI traffic from ChatGPT and Perplexity combined grew from 0.01% of organic traffic globally in 2024 to 0.13% in 2025 — four times the growth rate, but still four times almost nothing. The combined AI platform traffic grew 225% year on year. The absolute number remains a rounding error in most analytics dashboards.

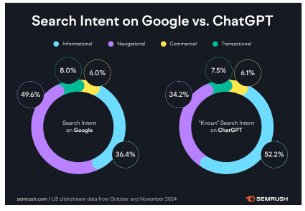

There is also an important structural point about the type of queries AI is handling. The evidence suggests — and the SEMrush intent data below supports this — that AI is disproportionately absorbing informational queries. Research, planning, writing assistance, general questions. Not the transactional searches that drive e-commerce revenue. Not "buy brown sofa" or "book a hotel in Edinburgh" or "compare home insurance." Those queries are still going to Google and converting.

Source: SEMrush — US clickstream data, October & November 2024. Transactional intent is significantly higher on ChatGPT, but the volume disparity means Google still handles the vast majority of converting queries.

The platforms that are actually changing behaviour

The more interesting story is not ChatGPT versus Google. It is the platforms that have quietly grown their role in the user journey without anyone declaring them an existential threat.

YouTube now has 2.58 billion monthly active users — roughly half the internet-using population. It generated $60 billion in revenue in 2025. People use it to research products before buying, to compare options, to watch reviews. It is a search engine for video intent, and it has been growing steadily for five years.

| Platform | MAUs 2020 | MAUs 2025/26 | Revenue 2025 |

|---|---|---|---|

| YouTube | 2.3bn | 2.58bn | $60bn |

| 459m | 619m (Q4 2025) | $4.2bn | |

| ChatGPT | 0 | ~500m (monthly) | ~$3.7bn |

Pinterest is the less obvious one — and arguably the more interesting one for e-commerce and lifestyle brands. It has grown from 459 million monthly active users in 2020 to 619 million in Q4 2025. It processes 80 billion searches a month, 96% of them unbranded. It is not tracked as a search engine by StatCounter because it does not sit in the same category — but functionally, for millions of users, it operates as one.

The key distinction: people go to Pinterest before they know what brand they want. They are searching for "dark green living room ideas" or "minimalist kitchen inspiration" — not for a specific product or retailer. That is the top of the funnel, and it is a long way upstream of Google. Brands that show up there are planting a flag before the purchase intent has fully formed.

What this actually means for SEO strategy

Two things. First: do not panic about Google. The share held, the revenue grew, and the types of queries that convert are still predominantly landing there. A well-optimised site with strong technical foundations, relevant content and genuine authority is still the right investment.

Second: understand where your customer is before they reach Google. For certain sectors — home, fashion, food, lifestyle, e-commerce broadly — there is a real question about whether YouTube and Pinterest deserve attention as part of a content strategy, not as social media channels but as search platforms with their own intent and optimisation requirements.

The user journey is multi-platform. It starts with inspiration (Pinterest, YouTube), moves through research (Google, YouTube), and ends with a transaction (Google, increasingly with AI-assisted comparison). Each platform serves a different intent at a different stage. Understanding which stage matters for your business — and being present there — is the strategy. Not chasing the platform that got the most LinkedIn posts this month.

The medium is still the message. Google is still the medium that converts. But the message is being shaped elsewhere first — and that is the part most strategies are missing.